In response to mounting financial pressures of Western sanctions, Russia enacted significant legislation legalizing cryptocurrency mining and permitting the use of cryptocurrency for international payments. The bills were signed into law on August 8th by President Vladmir Putin and crypto payment trials are slated to start this month, according to a Bloomberg report.

This represents a significant departure from the government’s previous stance in the country, where the Central Bank of Russia (CBR) had pushed for a complete ban on cryptocurrencies as recently as 2022. The new laws, set to take effect in September for cross-border payments and November for crypto mining, will enable Russian businesses to engage in international trade using cryptocurrencies and authorize approved entities to mine digital assets.

Putin has called on Russia “not to miss the moment” in regulating cryptocurrencies, emphasizing their growing role in global payments and potential to reduce reliance on the U.S. dollar. Key officials, including bill author Anton Gorelkin and CBR Governor Elvira Nabiullina, have specifically acknowledged that this legislative change is aimed at mitigating the impact of sanctions and facilitating international payments.

Russia’s evolving attitude towards cryptocurrency

Despite the recent legislation, Russia’s ban on using cryptocurrencies for domestic payments remains in place. Nevertheless, this has not dampened the widespread use of cryptocurrency within the country. In fact, Russia consistently ranks among the top countries in our annual Global Crypto Adoption Index, consistent with our broader observation that blanket bans on cryptocurrency are often ineffective, as they do not significantly curb usage but rather push it into informal or less regulated channels.

Concurrently, crypto-linked banking services have also been on the rise in Russia prior to the recent legislation. Rosbank, owned by Russian billionaire Vladimir Potanin, paved the way for cross-border cryptocurrency payments for business in June of last year, according to Vedomosti, with several other banks subsequently introducing similar services.

Sanctions evasion through cross-border payments

The CBR is spearheading the initiative to integrate cryptocurrency into Russia’s financial system for cross-border payments, creating an experimental infrastructure that allows approved Russian businesses and entities to use digital currencies for international trade. Approved mining entities will also be allowed to use crypto to settle trades, according to official statements.

These recent crypto-forward legislative efforts are part of Russia’s broader efforts to develop alternative payments mechanisms to alleviate Western sanctions pressure while decreasing dependence on the U.S. dollar, which has been a long-term goal for Russia especially amidst increasing geopolitical tensions.

The Central Bank of Russia: New scope of regulatory power

The new legislation consolidates the CBR’s control over cryptocurrency within Russia, enabling it to regulate and monitor these transactions closely. While the CBR is still testing its central bank digital currency (CBDC) with the digital ruble projected to launch in 2025, this legislation allows the use of existing cryptocurrencies with central bank oversight.

Russia has been exploring various methods to circumvent the U.S. dominated financial system, including blockchain-based initiatives with the BRICS community and the potential launch of a gold-backed stablecoin with Iran. The Financial Messaging System of the Central Bank of Russia (SPFS) — Russia’s alternative to the SWIFT financial messaging system — is another key component of this strategy, although its use remains limited.

Exchanges that may process international transactions

Per the Bloomberg report, authorities are exploring ways to legalize crypto exchanges. “We haven’t found a solution yet on how to do this,” said Finance Minister Anton Siluanov. Nevertheless, according to reporting by Russian news outlet Kommersant, Russia is moving forward with plans to launch two new crypto exchanges in St. Petersburg and Moscow. The exchange in St. Petersburg will reportedly be supported by infrastructure from the St. Petersburg Currency Exchange (SPCE), though SPCE has denied involvement according to the state-run news agency Interfax. Despite the regulatory ambivalence, Russia is already home to a thriving cryptocurrency ecosystem.

Some of Russia’s largest non-KYC exchanges, such as Tetchange, 100btc, Bitzlato, Suex, and Garantex, have been housed in or near Federation Tower, a two skyscraper complex located within the Moscow International Business Center, also known as Moscow-City. While some of these services, like Suex OTC, have seen a decline in activity following their designation by the U.S. Treasury Department, others, such as Garantex, have maintained a steady level of operations.

Garantex is a central player in Russia’s crypto market and likely to remain instrumental despite its designation by the Office of Foreign Assets Control (OFAC) and Office of Financial Sanctions Implementation (OFSI) in the U.S. and UK, respectively. This centralized exchange (CEX) has processed a substantial volume of transactions by designated actors in Russia and Iran, demonstrating its utility for sanctions evasion. Under the new legislation, the Russian government could officially or unofficially leverage services like Garantex, given its deep liquidity across major blockchains. Although Garantex has processed nearly $100 billion in transactions since 2018, this large-scale activity does not necessarily equate to state-sponsored sanctions evasion at scale, and should be assessed with caution. It’s important to note that not all Garantex users are Russian nationals or Russia-based, nor do they operate on behalf of the Russian government. Additionally, a great deal of sanctions evasion activity occurs outside official government channels and takes place through traditional off-chain methods, such as private investment vehicles and offshore shell companies.

Another exchange that could be leveraged for crypto-based sanctions evasion is Exved, which has worked closely with InDeFi Bank, co-founded by Garantex founder Sergey Mendeleev and former KGB officer and media tycoon Alexander Lebedev. Exved has been facilitating imports and exports even before the new legislation.

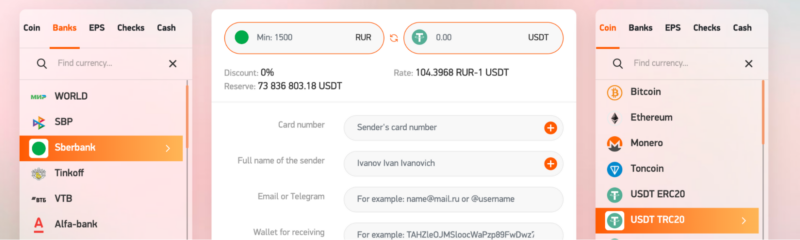

Note: This screenshot has been machine translated from the original Russian.

Additionally, InDeFi, which offers a broad range of DeFi products such as yield farming and flash loans, has been involved in efforts to launch a ruble-backed stablecoin on the Ethereum network, according to an InDeFi whitepaper and press reports.

Cryptocurrency businesses in Russia have had mixed success against the backdrop of the evolving legislative position. On one hand, Garantex represents a success story, while other global exchanges have exited the Russian market citing compliance concerns, with some local exchanges shuttering entirely. Last year, Binance sold its Russian operations to CommEX, which suspended its services earlier this year, reflecting the broader challenges of doing business in Russia after the February 2022 full-scale invasion of Ukraine.

Although it can be hard to quantify the true impact of certain sanctions actions, the fact that Russian officials have singled out the effect of sanctions on Moscow’s ability to process cross-border trade suggests that the impact felt is great enough to incite urgency to legitimize and invest in alternative payment channels it once decried.

Cryptocurrencies that could be used for payments

Russia is planning on launching Chinese Renminbi (RMB) Yuan and BRICS-based stablecoins, according to Kommersant, supported by the new crypto exchanges in development in St. Petersburg and Moscow. Additionally, the use of centralized stablecoins like USDT and USDC might also be considered given their liquidity and widespread global popularity, but their centralized control and regulatory responsiveness pose risks of disruption. The digital ruble could also play a role once launched, but given the heavy economic sanctions against Russia, its desirability to other countries remains uncertain. Finally, entities permitted to mine probably would do so in bitcoin, which remains deeply liquid and popular worldwide.

Scaling challenges of on-chain sanctions evasion

Russia’s move to integrate crypto into its financial system may improve its ability to bypass the U.S.-led financial system and to engage in non-dollar denominated trade. However, on-chain sanctions evasion at scale remains highly improbable, given Russia’s total foreign exchange reserves are just under half a trillion dollars, with approximately $300 billion in dollars, euros, and British pounds still frozen. As we have explored previously, current crypto markets simply do not have the liquidity to accommodate such large-scale transactions.

While large-scale sanctions evasion at the national level is unlikely, smaller-scale sanctions evasion on-chain can still have meaningful implications for national security, compliance, and investigations. Government-affiliated actors who might seek to leverage the new developments include fundraisers supporting pro-Russian militants in Ukraine, facilitators helping oligarchs and other politically exposed persons engage in capital flight, or Russian-language instant exchangers with no KYC requirements, servicing on- and off-ramping activities for sanctioned Russian banks. These smaller-scale activities can have major repercussions, highlighting the broader security and compliance risks associated with such transactions.

Below, we can see the interface of a Russian instant exchanger.

Users are able to transfer funds from their accounts at sanctioned Russian banks, like Sberbank, without performing any KYC and receive crypto in exchange. This means that users can effectively avoid fiat bans impacting sanctioned Russian banks.

Russia’s about-face on cryptocurrency represents a calculated response to Western sanctions, setting sights on an alternative financial system less dependent on the U.S. dollar. The success of this initiative will depend on how effectively Russia can navigate regulatory obstacles, manage sanctioned entities, and build the necessary infrastructure and foreign partnerships to support these transactions.

Implications of the crypto mining bill

Beyond bolstering the economy in wartime, Russia is positioning itself in an attempt to surpass the United States as the global leader in cryptocurrency mining.

The recently passed crypto mining bill introduces a structured framework for cryptocurrency mining, creating a register that allows Russian legal entities and entrepreneurs to engage in mining activities. This framework is designed to regulate mining operations with significant volumes, while smaller mining businesses under a set energy consumption limit will remain unaccounted for. The removal of language contained in an earlier draft of the mining bill suggests that the authorities may have sought to avoid taking action that would adversely affect Russia’s robust cryptocurrency ecosystem. In particular, the Kremlin-aligned Russian news outlet RBC has reported that a proposed ban on organizing cryptocurrency trading was removed from the law’s final version, avoiding a potential shutdown of Russian CEXs and providing a legal pathway for miners to monetize their activities.

Miners operating under the new law will be required to report their activities to the local financial monitoring service, Rosfinmonitoring, and to provide their wallet addresses to the security services, effectively legitimizing their operations under state oversight. This regulatory move raises important questions about the classification of crypto mining outside Russia as well, particularly in light of broad U.S. sectoral and European sanctions against Russia’s energy sector. Russia’s authorization and oversight of crypto mining suggests a strategic alignment with national interests, despite the ongoing international sanctions targeting Russia’s energy resources.

What’s next: Implications for authorities, VASPs, and TradFi

Although these legislative changes are likely to enhance Russia’s ability to engage in international trade through cryptocurrency, they are also likely to heighten vigilance among U.S. and EU authorities — particularly concerning counterparty risks and connections to some of Russia’s more important trade partners, like China and Iran. As these bills increase connectivity in global trade, Western authorities will likely remain focused on monitoring and mitigating risks associated with the financial activities of sanctioned entities, on- and off-chain.

More broadly, many heavily sanctioned countries, from Venezuela to Russia to Iran, have historically attempted to use alternative payment mechanisms, including cryptocurrency, to bypass sanctions — an approach fraught with challenges. The transparency of blockchain technology allows investigators to monitor and disrupt the movement of funds in real-time. Wallet addresses associated with CEXs, mining services, and other on-chain entities can be identified, attributed, and potentially sanctioned. Moreover, the liquidity limits of the cryptocurrency market mean that attempting to move large amounts of assets on-chain could either draw attention from blockchain observers or destabilize the market altogether.

For virtual asset service providers (VASPs) and traditional financial institutions, these developments underscore the importance of enhanced due diligence on counterparties of Russian mining entities. Overall, these changes make dealing with Russia-based entities even more challenging for CEXs, aligning with the broader trend of de-risking and debanking Russia since its full-scale invasion of Ukraine.

Chainalysis’ on-chain data, monitoring, and suite of investigative tools enable investigators and compliance professionals to proactively monitor these networks and take disruptive actions, making it increasingly difficult for designated entities to abuse cryptocurrency for sanctions evasion.

Timeline of Russia’s Shifting Positions on Digital Assets

| February 2020 | CBR tells pro-Kremlin newspaper Izvestia that a digital ruble could help reduce reliance on the dollar and increase resilience in the face of sanctions |

| October 2020 | CBR announces plans to release prototype CBDC in 2021 |

| June 2021 | CBR announces partnership with twelve major Russian banks, including Sberbank, VTB, Gazprombank, and Alfa Bank. |

| Fall 2021 | OFAC designates Russian OTC Suex and Russian CEX Chatex for facilitating cryptocurrency transactions for ransomware actors |

| January 2022 | CBR pushes for a blanket ban on the use and creation of cryptocurrencies, with Governor Elvira Nabiullina arguing they pose major risks to financial stability and economic security. The CBR said crypto resembled a pyramid scheme and singles out mining as a particular concern. The Russian Security Service (FSB) was reported to be advocating for the ban, saying that Russians were using crypto to donate to undesirable organizations and ‘foreign agents.’ |

| February 2022 | CBR announces that it has created a prototype of the digital ruble platform, and that two partner banks had successfully completed a full cycle of digital ruble transfers in late 2021 through mobile banking applications. |

| 18 February 2022 | Ministry of Finance introduces a crypto bill, proposing a licensing regime for the platforms facilitating the circulation of digital assets and stipulating prudential, risk management, data privacy and reporting requirements for VASPs. |

| 24 February 2022 | Russia launches full-scale invasion of Ukraine |

| Late February-Early March 2022 | US, EU, and other Western allies freeze around $300 billion in sovereign reserves |

| 12 March 2022 | SWIFT bans seven Russian banks and their subsidiaries |

| 5 April 2022 | OFAC designates Russian CEX Garantex for facilitating crypto-based money laundering for ransomware actors |

| December 2023 | US launches new secondary sanctions authority on foreign financial institutions transacting with US-designated Russian entities

Banks in Turkey, the UAE, and China ask clients to provide written assurances that recipients of payments are not on OFAC’s SDN list |

| February 2024 | Three Chinese banks (ICBC, China Construction Bank, and Bank of China) stop accepting payments from designated Russian FIs |

| May 2024 | Iran confirms having worked with Russia to address settlements using CBDCs. |

| Early July 2024 | Putin calls cryptocurrencies “a very dynamic and promising direction of the modern economy.”

CBR Governor Nabiullina cites payments issues as one of the main challenges facing Russia’s economy amid Chinese banks’ increased caution on payments with Russian counterparts |

| 30 July 2024 | Duma passes two laws, one legalizing virtual currency mining and the other paving the way for the use of crypto for international payments. |

| 8 August 2024 | Crypto payments and mining bills are signed into law by President Vladmir Putin |

| September 2024 | Crypto payment trials slated to begin |

| (Estimated) July 2025 | Target date for widespread implementation of the digital ruble (retail and wholesale) |

This website contains links to third-party sites that are not under the control of Chainalysis, Inc. or its affiliates (collectively “Chainalysis”). Access to such information does not imply association with, endorsement of, approval of, or recommendation by Chainalysis of the site or its operators, and Chainalysis is not responsible for the products, services, or other content hosted therein.

This material is for informational purposes only, and is not intended to provide legal, tax, financial, or investment advice. Recipients should consult their own advisors before making these types of decisions. Chainalysis has no responsibility or liability for any decision made or any other acts or omissions in connection with Recipient’s use of this material.

Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information in this report and will not be responsible for any claim attributable to errors, omissions, or other inaccuracies of any part of such material.