Compliant cryptocurrency businesses know what it takes to keep their platforms safe: They need to conduct KYC checks on customers, monitor transactions for counterparty risk, implement anti-money laundering (AML) policies, and file SARs when they see suspicious flow of funds. However, these can’t just be one-time jobs that only happen when a new customer signs up or when a transaction takes place. If new information comes out that raises a customer or counterparty’s risk factor — like news of possible involvement in financial crime or an OFAC designation — then previous transactions involving that person or entity retroactively become risky even if they initially appeared safe. Those old crypto transactions may therefore warrant a suspicious activity report (SAR) or other actions by the compliance team, such as taking additional anti-money laundering measures.

Therein lies the value of continuous cryptocurrency transaction monitoring: it’s the best way for compliance teams to identify and respond to historical transactions that are later reclassified as high-risk. This forms the foundation of any effective anti-money laundering program.

Below, we explain why continuous monitoring is important and show you how Chainalysis KYT (Know Your Transaction) makes it easy.

Why continuous cryptocurrency transaction monitoring is necessary

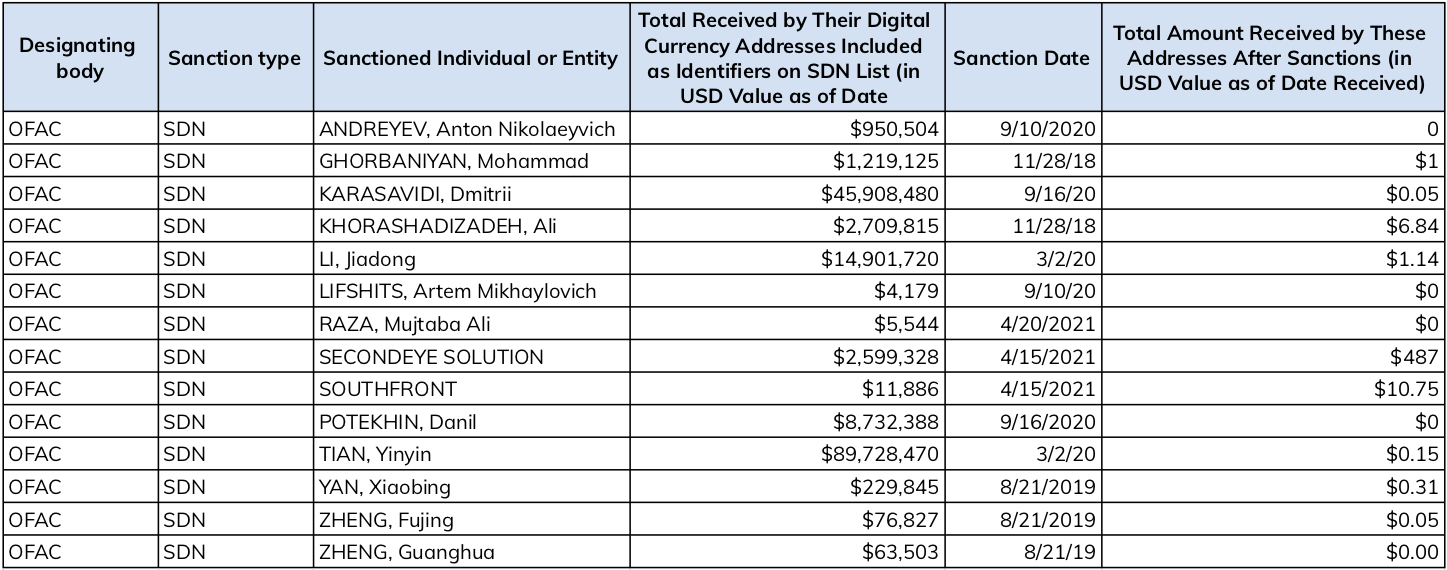

Sanctioned individuals and entities represent some of the biggest compliance risks for both crypto businesses and mainstream financial institutions. Since 2018, the U.S. Treasury’s Office of Foreign Assets Control (OFAC) has included cryptocurrency addresses in the Specially Designated Nationals (SDN) list entries for a handful of sanctioned entities, including developers of destructive ransomware strains and individuals found to have laundered funds on behalf of cybercriminals associated with the North Korean government.

Blockchain analysis suggests that cryptocurrency compliance teams have been effective in helping enforce these sanctions.

Every sanctioned entity with an OFAC-identified cryptocurrency address has received little to no cryptocurrency payments since being added to the SDN list. However, that doesn’t mean compliance teams’ work is done. In addition to preventing future payments, cryptocurrency compliance teams need to review past transaction activity when a new entity is sanctioned to see if their platform previously processed transactions with that entity, even if the compliance team would have had no way of knowing about upcoming sanctions when those transactions occurred. If reviews showed their platform did transact with that now-sanctioned entity, the compliance team would need to report those transactions through the appropriate channels.

Keep in mind, this doesn’t just apply to sanctioned entities, but to any entity whose virtual asset transaction activity becomes suspicious in hindsight. For instance, if a Bitcoin wallet was identified as belonging to a ransomware operator, cryptocurrency exchange compliance teams would need to identify any old transactions occurring between that ransomware wallet and addresses hosted by their platform. Compliance teams who don’t continuously monitor for newly identified risk in old transactions could find themselves in trouble with regulators, who are themselves adopting the blockchain analysis platforms compliance teams rely on, and can therefore spot historic suspicious activity that compliance teams fail to report.

What effective continuous monitoring looks like

Any continuous cryptocurrency transaction monitoring solution needs three elements to be effective for compliance teams.

Automatic alerts

It would be so time-consuming as to be infeasible for compliance teams to manually screen old transactions on a consistent basis as they learn about new risk factors. Luckily, that’s not necessary. With the right architecture in place, once a blockchain data platform has attributed new risk designations for old wallets, it can scan the blockchain to spot any suspicious transactions between those wallets and a cryptocurrency platform, and notify the platform’s compliance team via real-time transaction monitoring alerts.

Customized alert thresholds

Some transactions with risky entities aren’t large enough to create real risk or warrant a follow-up from compliance, and these standards change from one organization to another based on differing policies and priorities. If your continuous monitoring tool doesn’t account for that, your compliance team could be inundated with non-critical alerts. A good continuous monitoring tool will let compliance teams set customized alert thresholds for risky transactions, with different thresholds for different risk categories, so that they only receive alerts for historic transactions that require a follow-up.

No extra fees

Some cryptocurrency compliance solutions support continuous monitoring, but require compliance teams to pay for the “re-screening” of old transactions. This is especially common with softwares that don’t provide automatic alerts and instead require manual re-screening. Not only do these unpredictable costs put a dent in compliance teams’ budgets, but it also makes the cryptocurrency ecosystem less safe by disincentivizing compliance teams from undertaking continuous monitoring in the first place. At Chainalysis, we don’t believe in imposing extra costs on workflows necessary for cryptocurrency platforms to meet the compliance requirements mandated by regulators.

Chainalysis KYT’s continuous monitoring checks all the boxes

A continuous monitoring tool with the three elements described above lets compliance teams rest easy, knowing that they’ll automatically learn when an old transaction becomes suspicious due to new information. Chainalysis KYT checks all the boxes. In addition to monitoring new transactions for risks as they occur in real time, its continuous monitoring tool has everything compliance teams need to get peace of mind when it comes to historic transactions.

Want to learn more? Contact us here to talk to someone on the team and learn how KYT can make your compliance team more effective.