This post is an excerpt from our 2024 Geography of Cryptocurrency Report. Reserve your copy now!

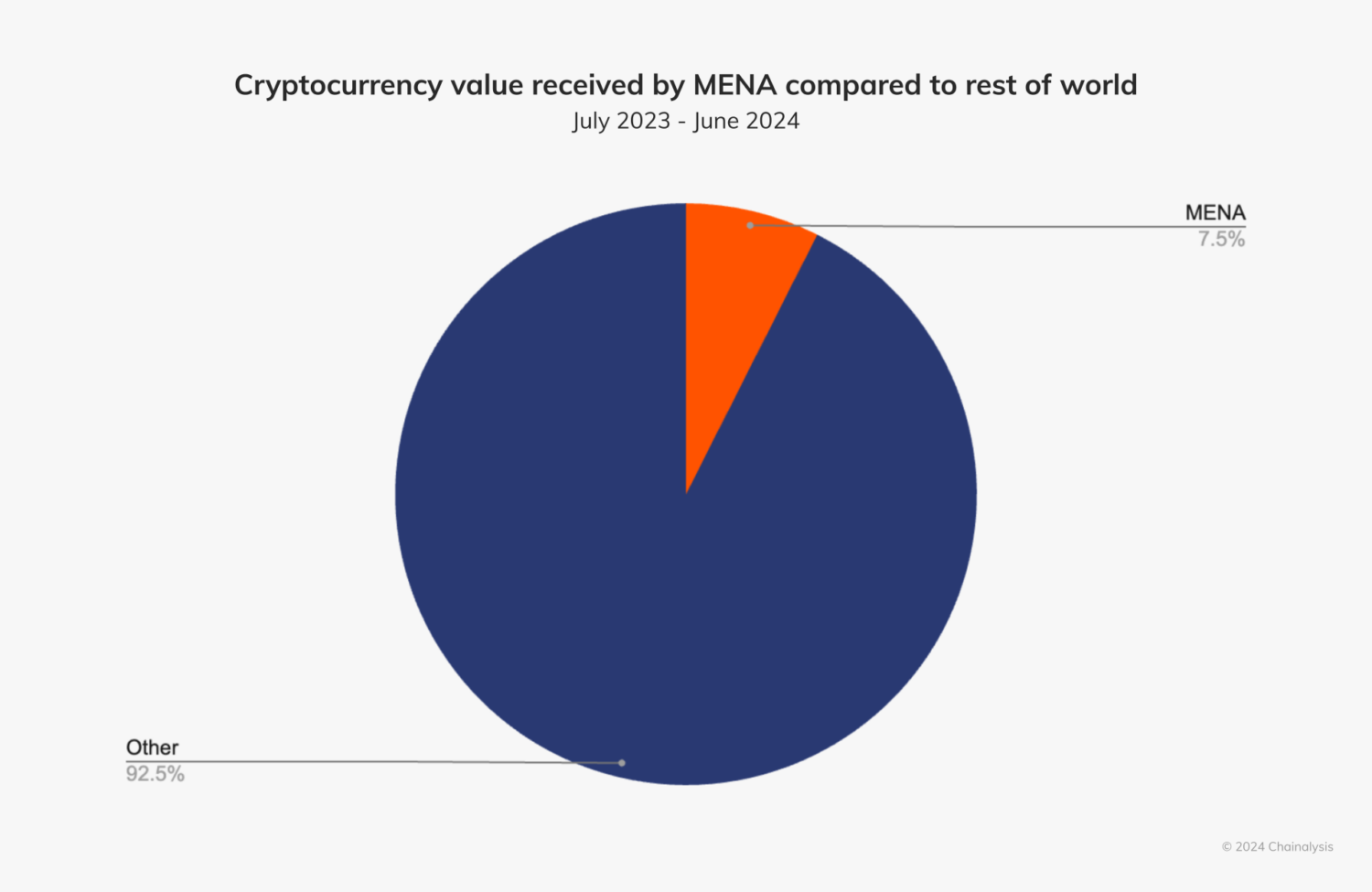

The Middle East & North Africa (MENA) region ranks as the seventh-largest crypto market globally in 2024, with an estimated $338.7 billion in on-chain value received between July 2023 and June 2024, accounting for 7.5% of the world’s total transaction volume.

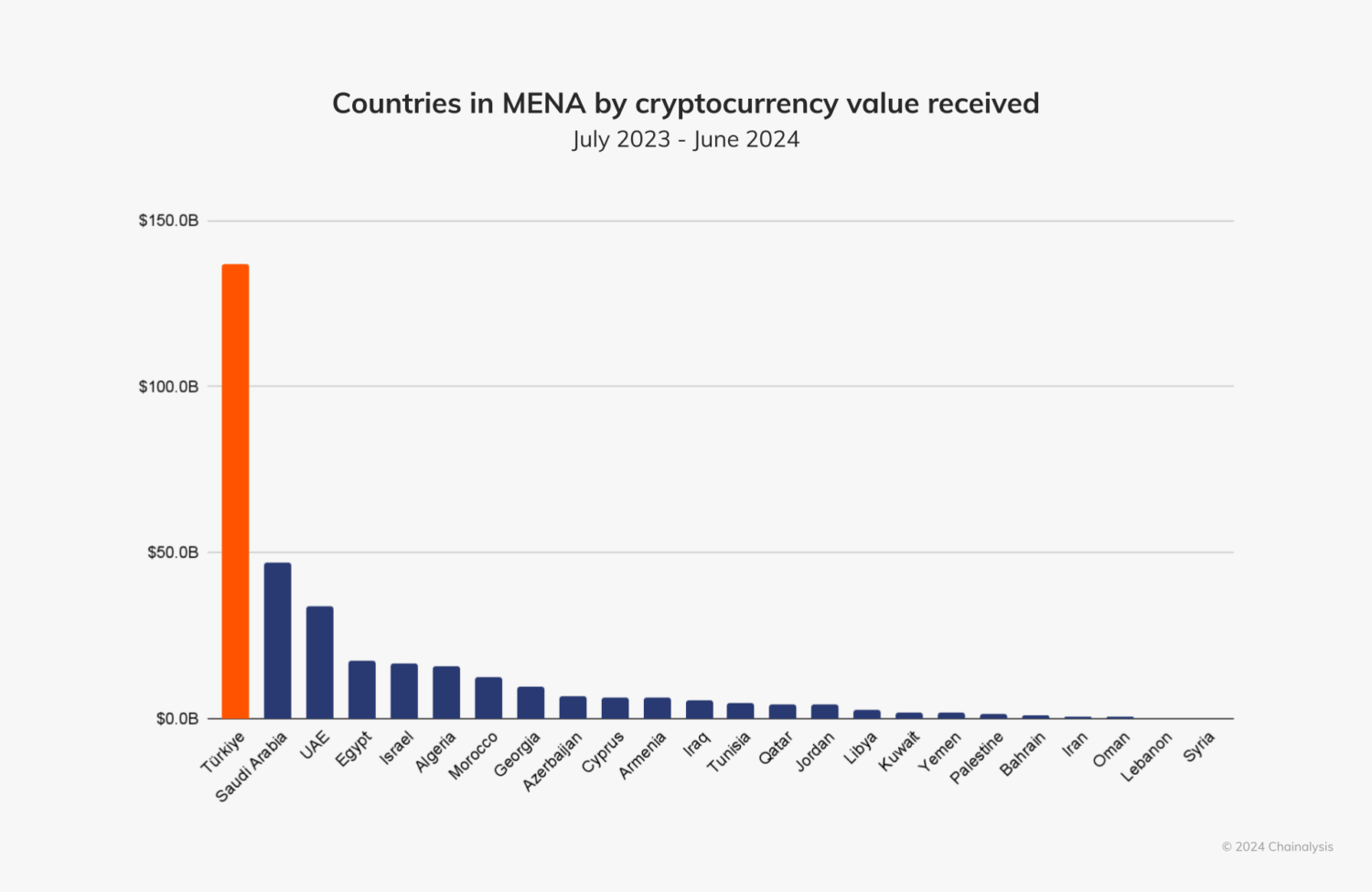

Although the market is smaller compared to other regions, MENA includes two countries ranked in the top 30 of the global crypto adoption index: Türkiye (11th) and Morocco (27th), capturing $137 billion and $12.7 billion of value received, respectively.

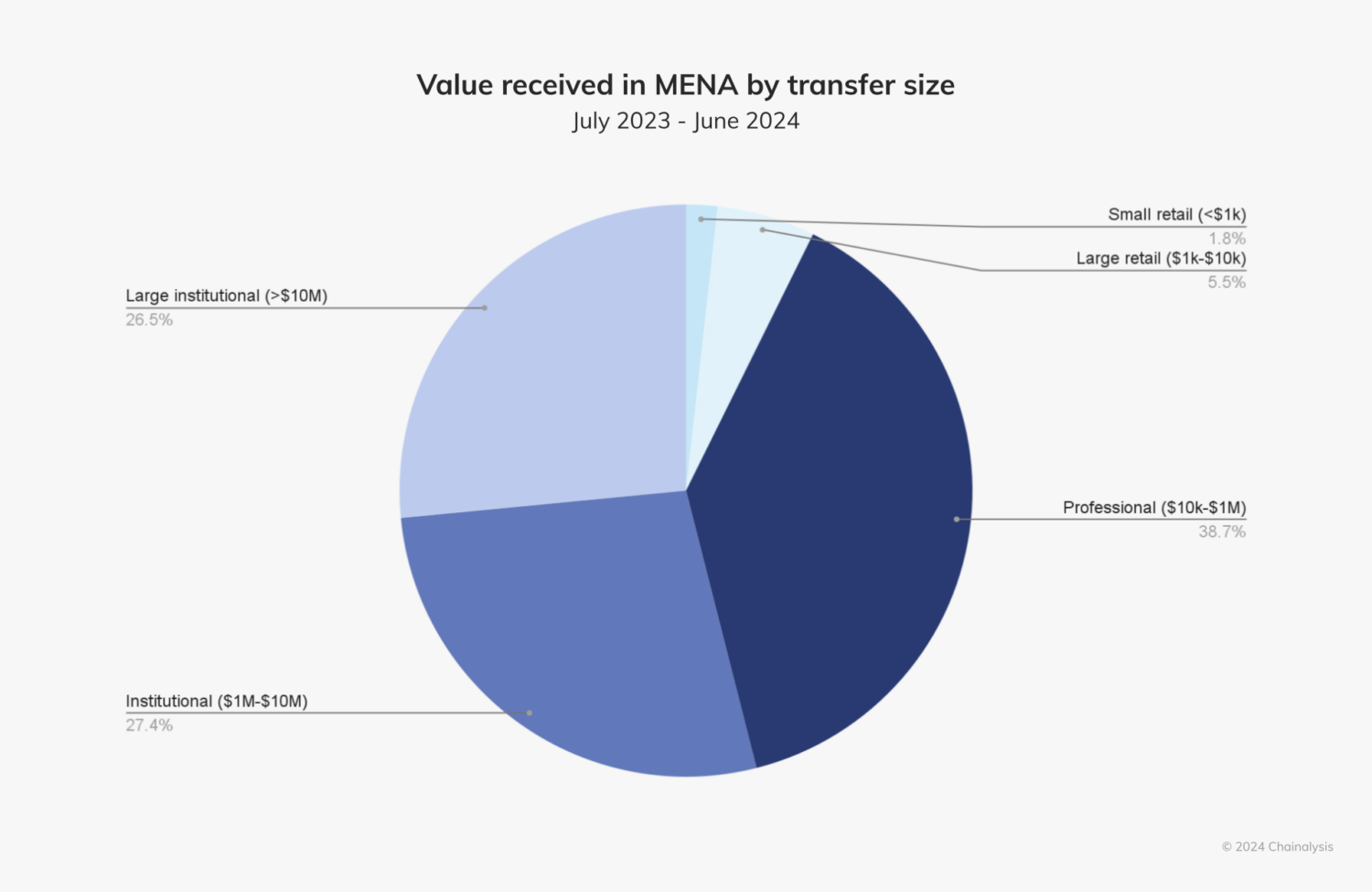

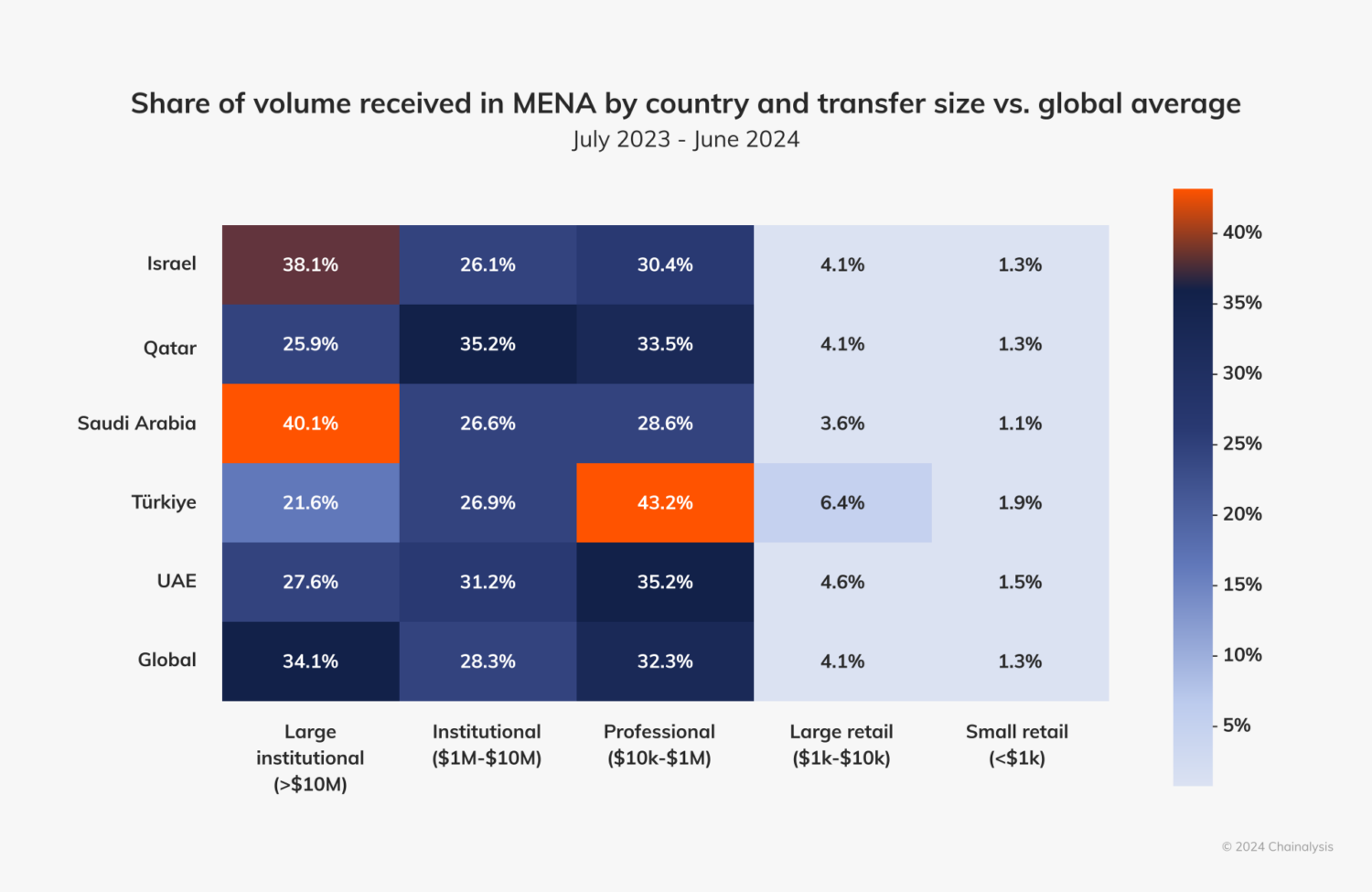

The majority of crypto activity in MENA is driven by institutional and professional-level activity, with 93% of value transferred consisting of transactions of $10,000 or above.

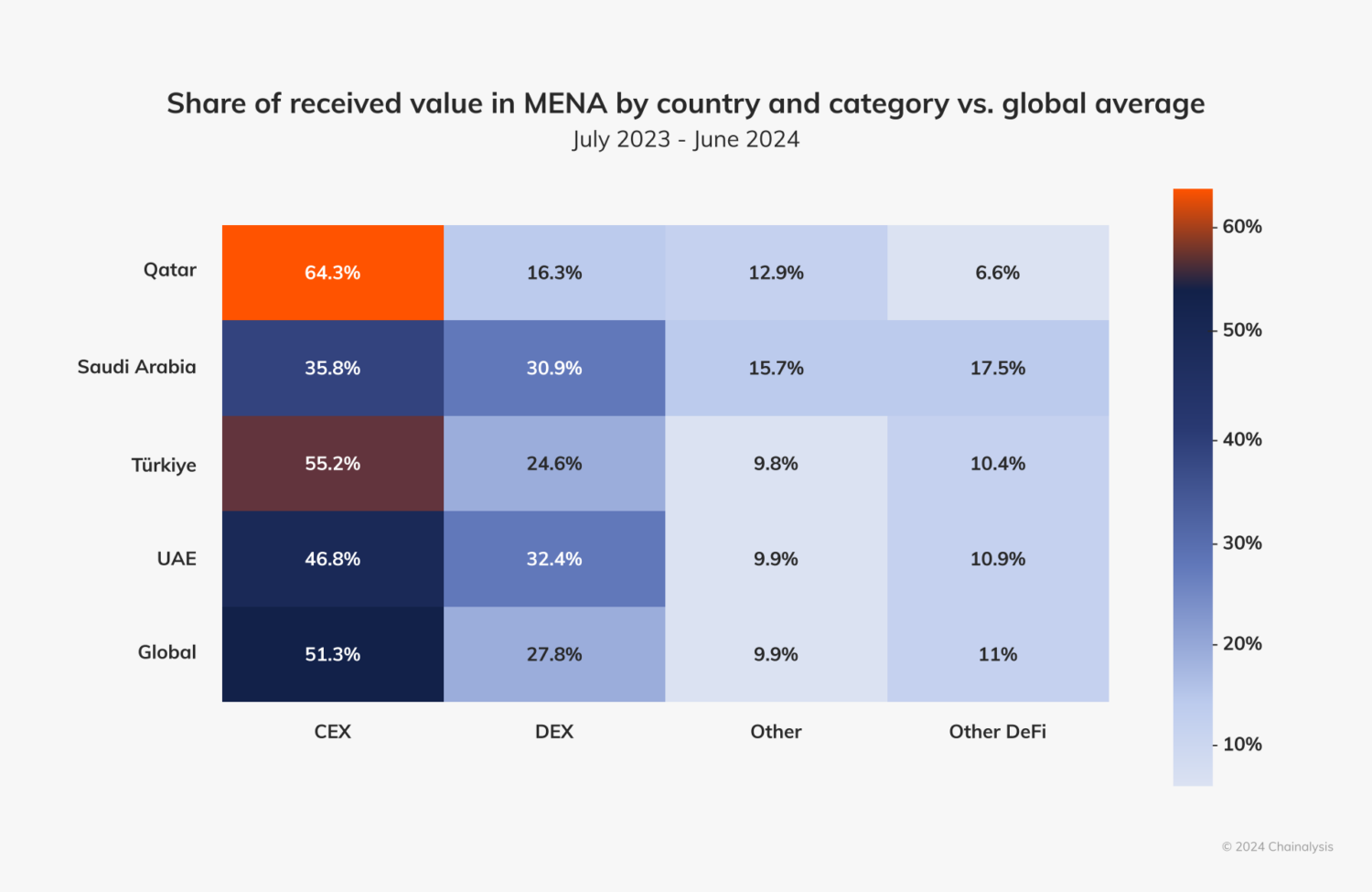

Centralized exchanges (CEXs) remain the primary source of crypto inflows across MENA overall, indicating that most users and institutions still prefer traditional crypto platforms, but decentralized platforms and DeFi applications are steadily gaining traction, as seen in the heatmap below.

Notably, Saudi Arabia and the UAE demonstrate high interest in decentralized platforms. The majority of DeFi activity across MENA occurs on DEXs, with Saudi Arabia participating in other DeFi activities at a marginally higher share than the other nations shown. Saudi Arabia, a G20 economy with a population of over 30 million, benefits from a disproportionately young population — around 63% of its citizens are under 30 years old. This demographic is especially meaningful from an emerging technology perspective, as younger generations tend to be more open to experimenting with new financial technologies. The UAE also shows higher DeFi adoption than the global average, likely attributable to its progressive regulatory stance which has fostered clarity around specific classes of crypto participation. The UAE’s proactive and collaborative regulatory approach to crypto and web3 companies has attracted a diverse range of users, and solidified the UAE as a hub for DeFi and broader crypto activity. In contrast, users in Türkiye and Qatar remain heavily reliant on CEXs, with lower DeFi participation compared to global averages.

It’s important to note that both Saudi Arabia and Qatar do not yet have a comprehensive regulatory framework in place for virtual asset service providers (VASPs) and therefore do not yet have local CEXs, but encouraging new developments in Qatar that allow companies to apply for a license to become token service providers could reshape the landscape in the future.

Beyond fostering innovation, DeFi offers an alternative financial system for the unbanked and underbanked, which is critical for a region where less than 50% of adults, excluding high-income economies, had a bank account as of 2021. While DeFi adoption may not yet be widespread in some of these regions, its ability to provide financial services without intermediaries could drive future financial inclusion, opening up new opportunities for individuals in underserved areas, and empowering them with access to loans, savings, and investment tools previously unavailable.

Regulatory strides made across key markets in the region in 2024 are likely to further shape the distribution of DeFi and CEX platforms, impacting financial inclusion and the broader adoption of decentralized financial systems.

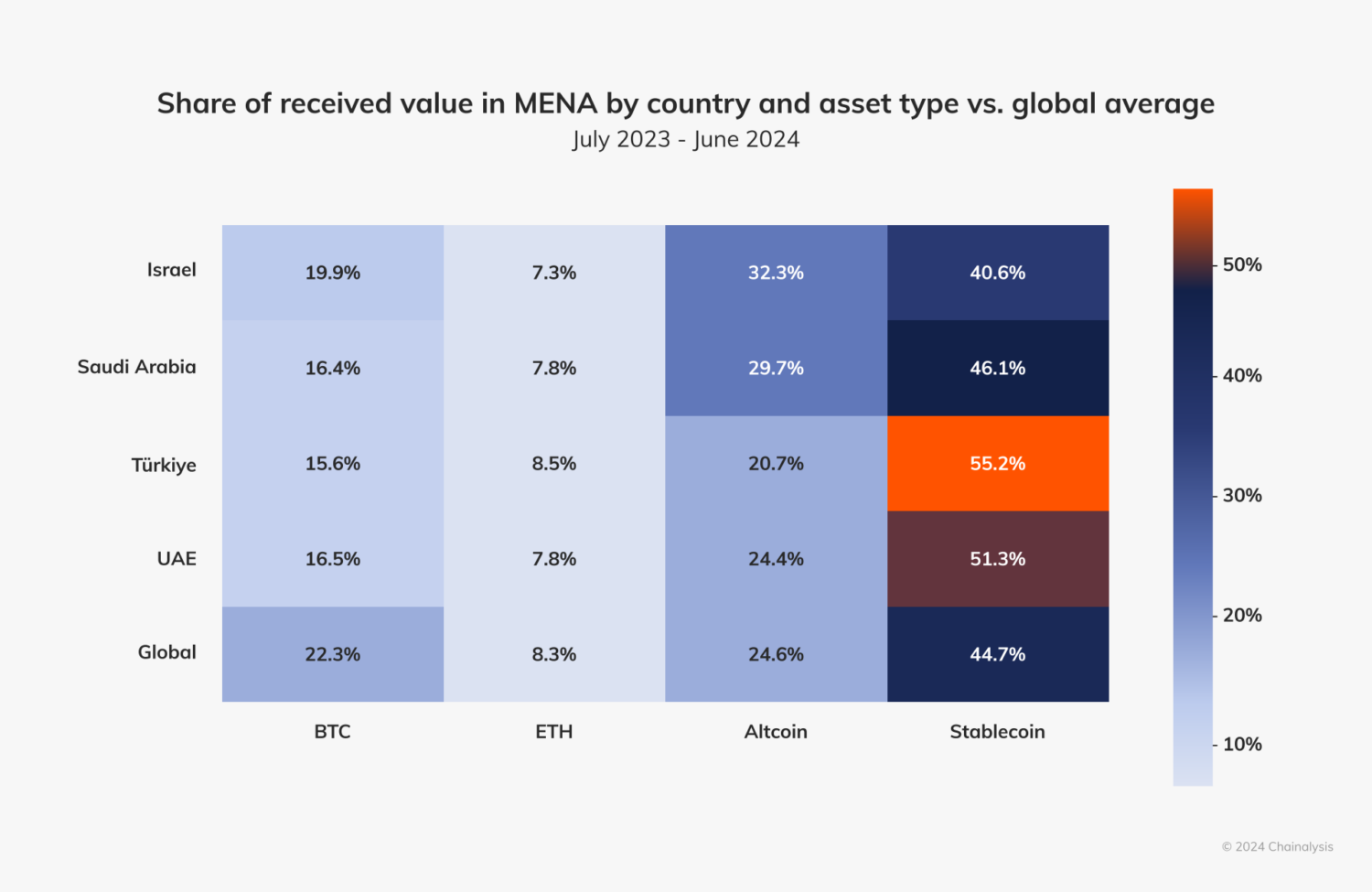

Stablecoins and altcoins making gains across MENA

Across MENA, stablecoins and altcoins are gaining market share over traditionally preferred assets like bitcoin and ether, particularly in Türkiye, Saudi Arabia, and the UAE, which have higher shares of stablecoin volume.

For example, in Türkiye, which has a long history of economic instability and high inflation, retail users’ reliance on stablecoins reflects their concerns over volatility and a need for consistent stores of value — which we detail further down. In contrast, in the UAE, where the local currency (the Emirati dirham) is pegged to the U.S. dollar, the growing adoption of stablecoins likely reflects their popularity as an on-ramp to broader crypto services and trading.

Ether (ETH) usage across the region is relatively consistent, but falls below the global average, with Türkiye leading in engagement. Meanwhile, Israel and Saudi Arabia demonstrate a strong interest in altcoins, well above the global average, possibly reflecting a higher risk appetite and interest in a wider variety of assets beyond the major cryptocurrencies. Last year, Israel completed a successful government bond tokenization pilot, aligning with broader industry interest surrounding tokenized assets — a sector which McKinsey predicts could reach $4 trillion by 2030.

Clear regulation drives a balanced crypto ecosystem in the UAE

The UAE continues to experience rapid growth in the crypto space, driven by a combination of regulatory innovation, institutional interest, and expanding market activity. Between July 2023 and June 2024, the UAE received over $30 billion in crypto, ranking the country among the top 40 globally in this regard and making it MENA’s third largest crypto economy.

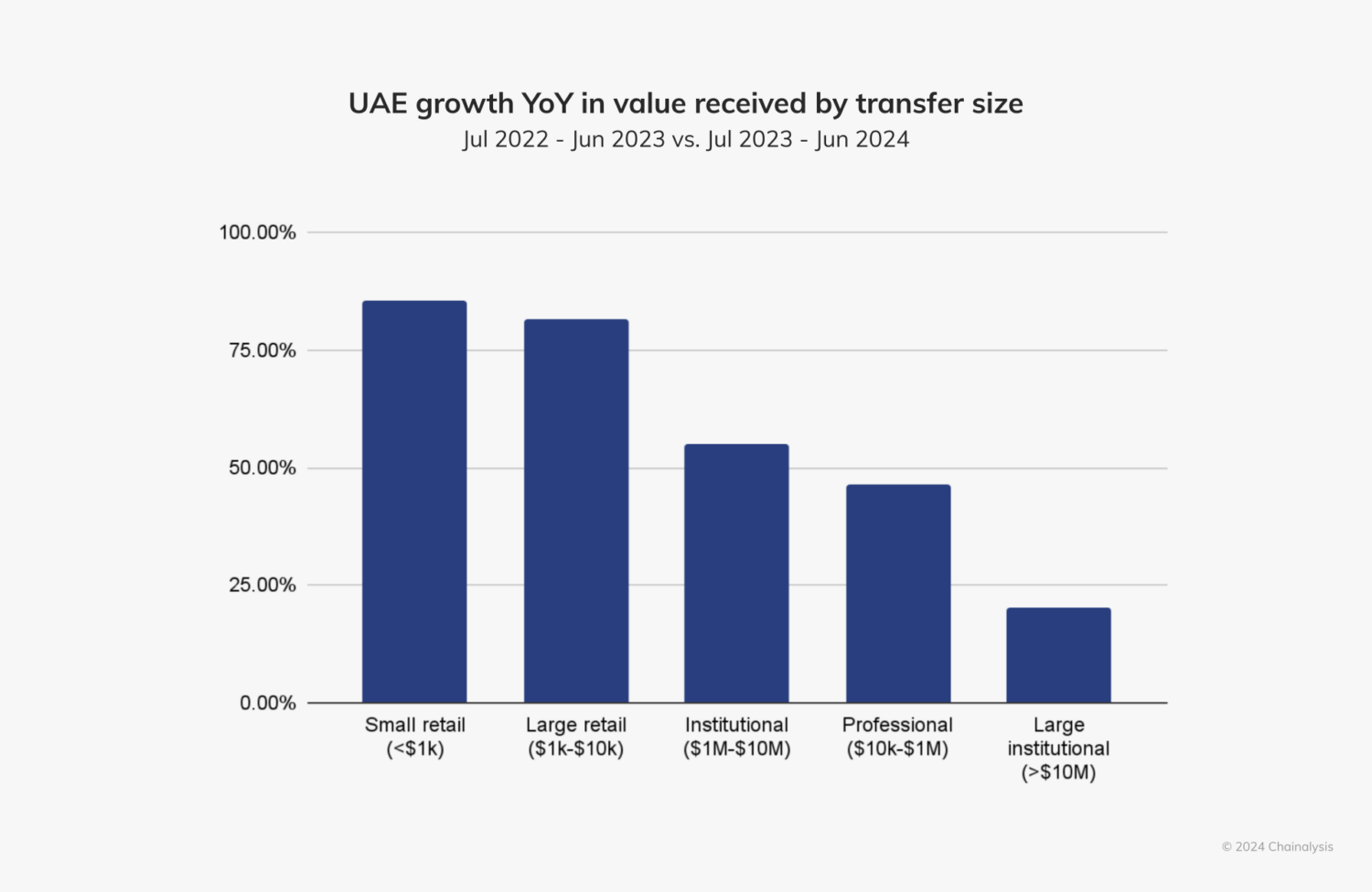

Unlike most countries globally, the UAE’s crypto activity is growing across all transaction size brackets, signaling a more balanced and comprehensive adoption landscape.

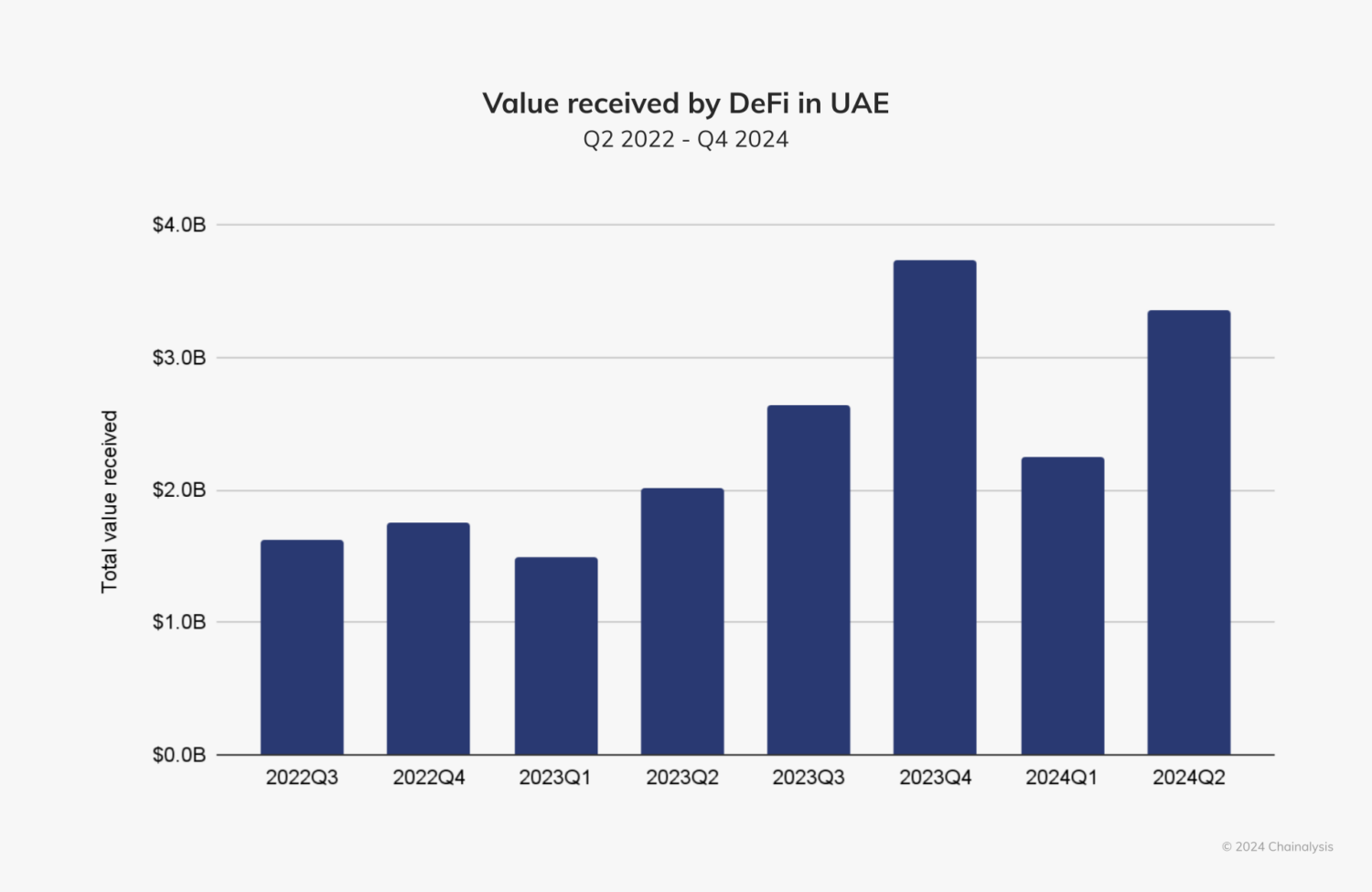

The country also boasts a diversified crypto ecosystem, with significant activity beyond CEXs, including DeFi.

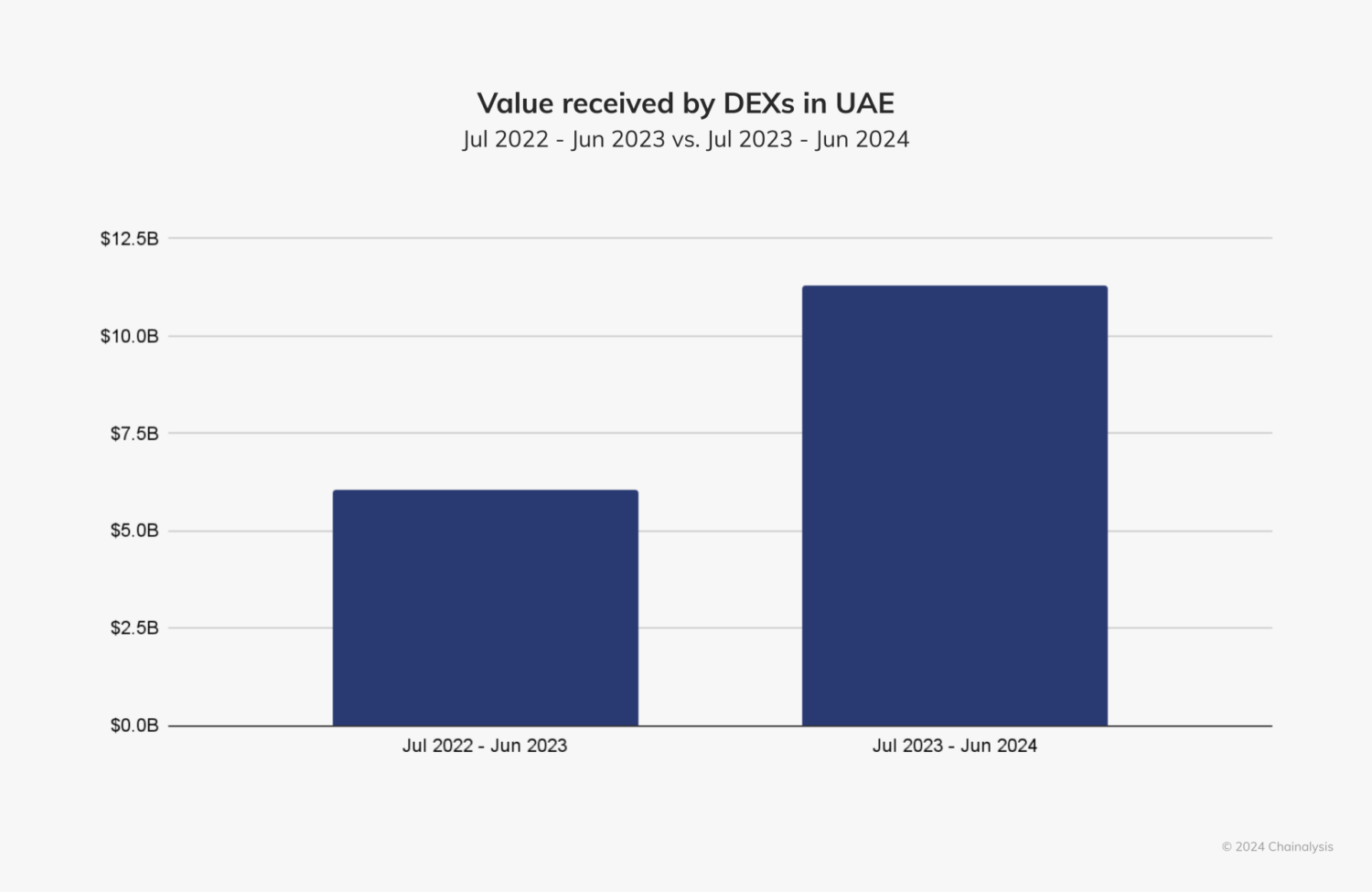

The total value received by DeFi services, including DEXs, grew by 74% compared to last year, and that received by DEXs alone grew by 87%, from an estimated $6 billion to $11.3 billion.

Crypto investments are also expanding quickly as numerous VC funds and blockchain businesses set up shop in the UAE — including Chainalysis, which debuted its regional headquarters in Dubai this May. Tether, the issuer of the world’s most traded cryptocurrency, also recently announced plans to launch a stablecoin pegged to the Dirham.

“Traditional financial institutions such as banks are actively exploring their roles within the crypto ecosystem, showcasing the growth of a crypto-TradFi nexus,” noted Arushi Goel, Head of Policy for the Middle East and Africa at Chainalysis. “This engagement is further supported by a robust and evolving regulatory framework.”

Indeed, as global crypto markets rebound, governments are working towards crafting regulatory frameworks that balance innovation with necessary safeguards. The UAE is at the forefront this effort, with various regulatory authorities across its Emirates developing tailored approaches. At the federal level, the Securities and Commodities Authority (SCA) regulates virtual assets services, while the Central Bank of the UAE (CBUAE) oversees payment token services. Additionally, the two financial free zones — the Dubai International Financial Centre (DIFC) and Abu Dhabi Global Market (ADGM) — operate independent financial regulatory regimes, each with its own distinct virtual asset asset framework.

Dubai’s Virtual Assets Regulatory Authority (VARA) is also playing a critical role in this regulatory expansion. Established in 2022 as the world’s first standalone regulator for virtual assets, VARA is not only shaping the local market, but also attracting global attention.

Deepa Raja Carbon, Managing Director and Vice Chairperson of VARA, spoke with Arushi Goel about the unique position VARA occupies as a regulator two years after its creation. “We’ve identified over a thousand entities conducting crypto-related activity within Dubai and we’re working through a legacy transition. Over the next year, we expect to see these entities licensed,” she explained, adding that VARA’s approach is one of collaboration rather than blind enforcement. “Both the industry and regulators come to the table with that perspective — to learn together and evolve,” she said, stressing the importance of balancing market protection with innovation.

VARA’s influence extends well beyond Dubai, as its regulatory framework sets a precedent for other jurisdictions. The UAE is actively positioning itself as a world leader in emerging technologies, making substantial investments in artificial intelligence (AI) and other advanced technology sectors to solidify its reputation as a global innovation hub. This strategic focus further amplifies its impact on the crypto ecosystem, where VARA’s collaborative innovation-focused approach is setting the tone. “It’s a fascinating time to be involved as a regulator,” added Carbon. “You’re able to witness game-changing ideas, while also providing the framework for them to be tested and brought to market more quickly than in a traditional sandbox.”

In Türkiye, stablecoins and high consumer engagement propel market maturation

Türkiye ranks as the largest crypto market in MENA and seventh globally, receiving $136.8 billion in value between July 2023 and June 2024.

This robust activity is fueled by an ecosystem defined by a strong presence of local CEXs and increasing expansion by global platforms, with 76 CASPs having declared their intent to comply with the regulatory regime, as of the date of this publication.

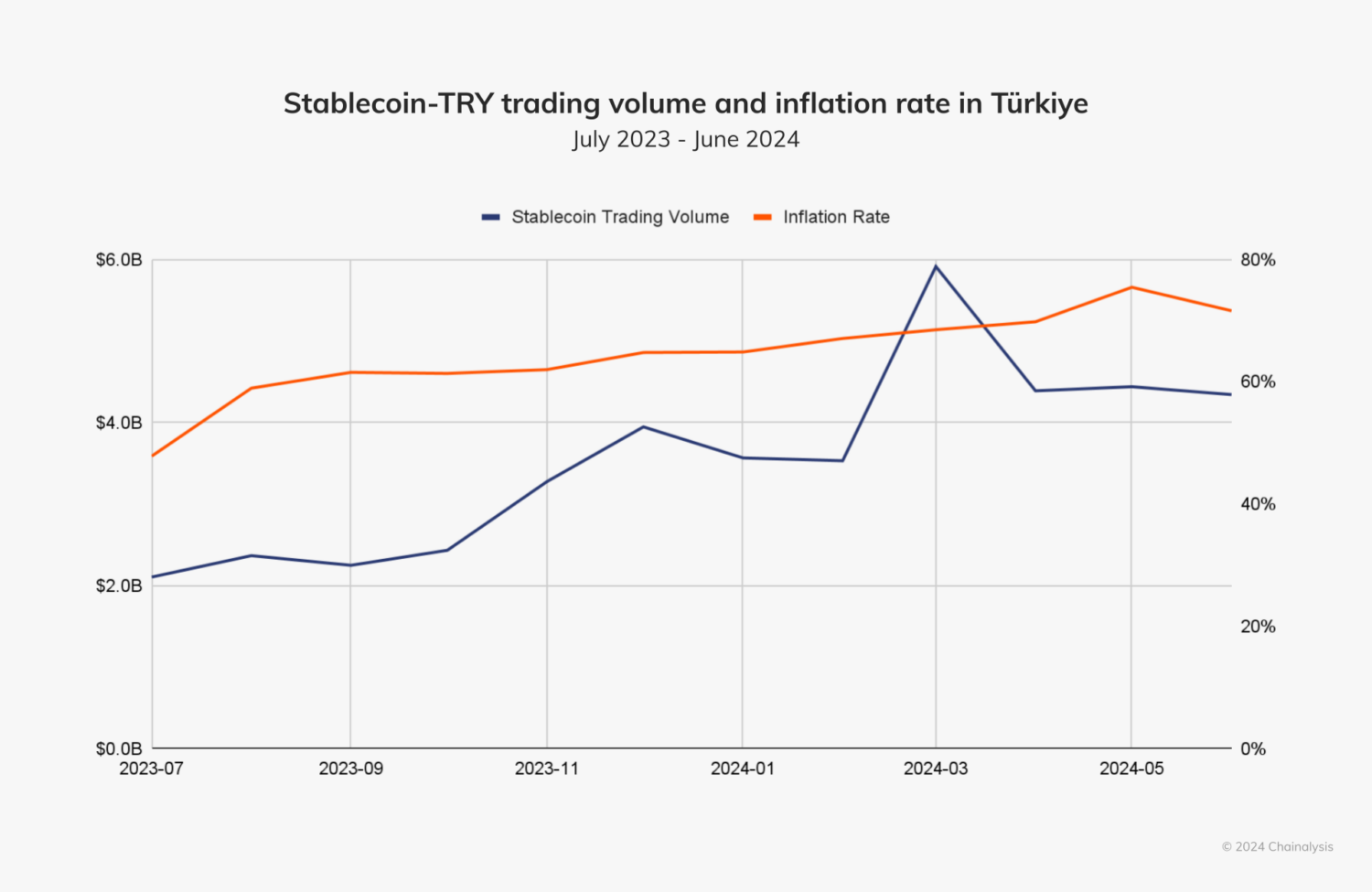

Additionally, as we covered in last year’s report, Türkiye’s high inflation rate, which has hovered near or above 50% for the past year, has driven much of the country’s crypto adoption. Amidst this high inflation, citizens have turned to cryptocurrencies — particularly stablecoins and altcoins — to hedge against currency devaluation and seek higher returns.

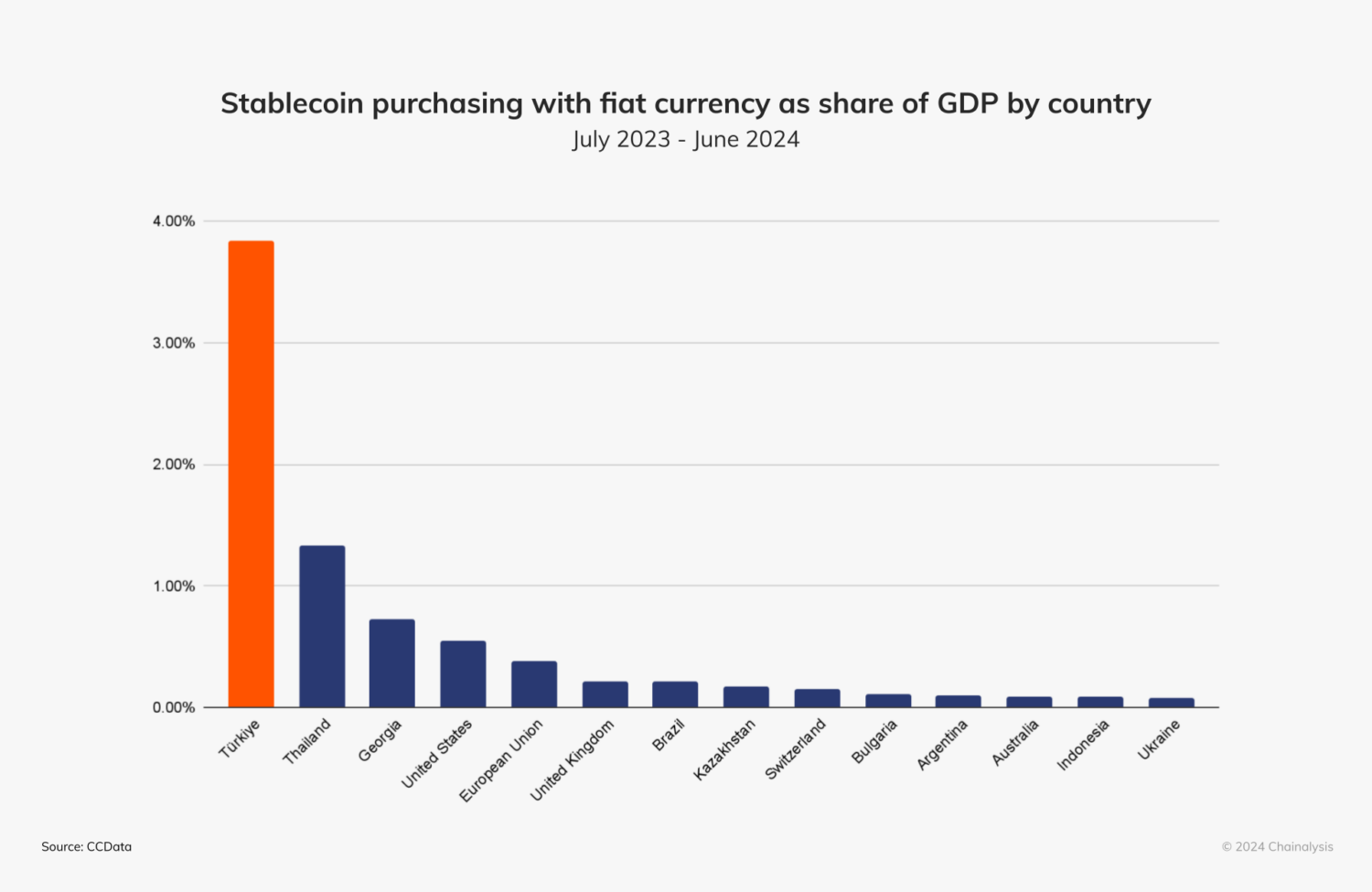

Crypto trading volume on order books can provide valuable insight on the popularity of a given asset. Türkiye is number one in the world in stablecoin trading volume as a percentage of GDP, by a large margin.

It’s important to note this measure is not saying that nearly 4% of Turkish GDP is stablecoins, but that stablecoin trading volumes on CEXs are equal to 4% of GDP in dollar equivalent terms, meaning crypto trading volumes could one day exceed a country’s measure of GDP.

Stablecoins consistently represent the majority of crypto assets purchased with the Turkish Lira, approaching nearly $6 billion in purchases in March of this year. As we see in the chart below, stablecoin purchases with the Turkish Lira are closely correlated with inflation rates.*

This mirrors a broader trend we have observed over the years in regions with monetary instability, where the demand for non-volatile assets, such as the U.S. dollar and dollar-pegged stablecoins, is high.

To gain further insight into Türkiye’s crypto landscape, we spoke with Francisco Maroto, Head of Blockchain at Banco Bilbao Vizcaya Argentaria (BBVA), a Spanish multinational financial services company with a presence in Türkiye. Maroto emphasized that Türkiye’s crypto adoption is largely customer-driven, estimating that 40% to 50% of the population is engaged in crypto. This high adoption rate is linked to the need for consumer financial protection amidst ongoing inflation, as well as an inclination toward riskier, high-reward tokens. “Apart from BTC and ETH, we see football team coins and fancy tokens in the top traded volumes,” Maroto explained, describing how Turkish users are more likely to invest in more speculative altcoins.

Garanti BBVA’s crypto strategy in Türkiye reflects the country’s growing demand for cryptocurrency. As regulations take shape, Garanti BBVA has been offering crypto custody services since early 2024 and is launching trading services soon. “We foresee more banks stepping into the market with new regulations,” Maroto noted, as Türkiye recently amended its Capital Markets Law to include crypto assets, with the objective of enhancing market integrity and consumer protection for the crypto ecosystem. While crypto markets in Türkiye have historically been dominated by exchanges like Binance and local CEXs such as Paribu, banks like Akbank and Garanti BBVA are now entering the space, aiming to provide regulated services, including custody and trading.

As Garanti BBVA expands its crypto offerings in Türkiye, both retail and institutional clients are driving demand. Retail users often use crypto for investment and as a hedge against inflation, while institutional users, primarily investment funds, are becoming more involved as the market matures. Türkiye stands out for having the highest share of professional-level crypto transactions (43.2%) in the MENA region, indicating a vibrant market for mid-sized transfers and large-scale retail activity.

BBVA’s focus on both retail and institutional customers speaks to the dynamic and rapidly evolving nature of Türkiye’s crypto landscape.

With further regulatory developments on the horizon, Türkiye’s crypto market is poised for further growth, potentially reshaping the regional and global crypto ecosystem.

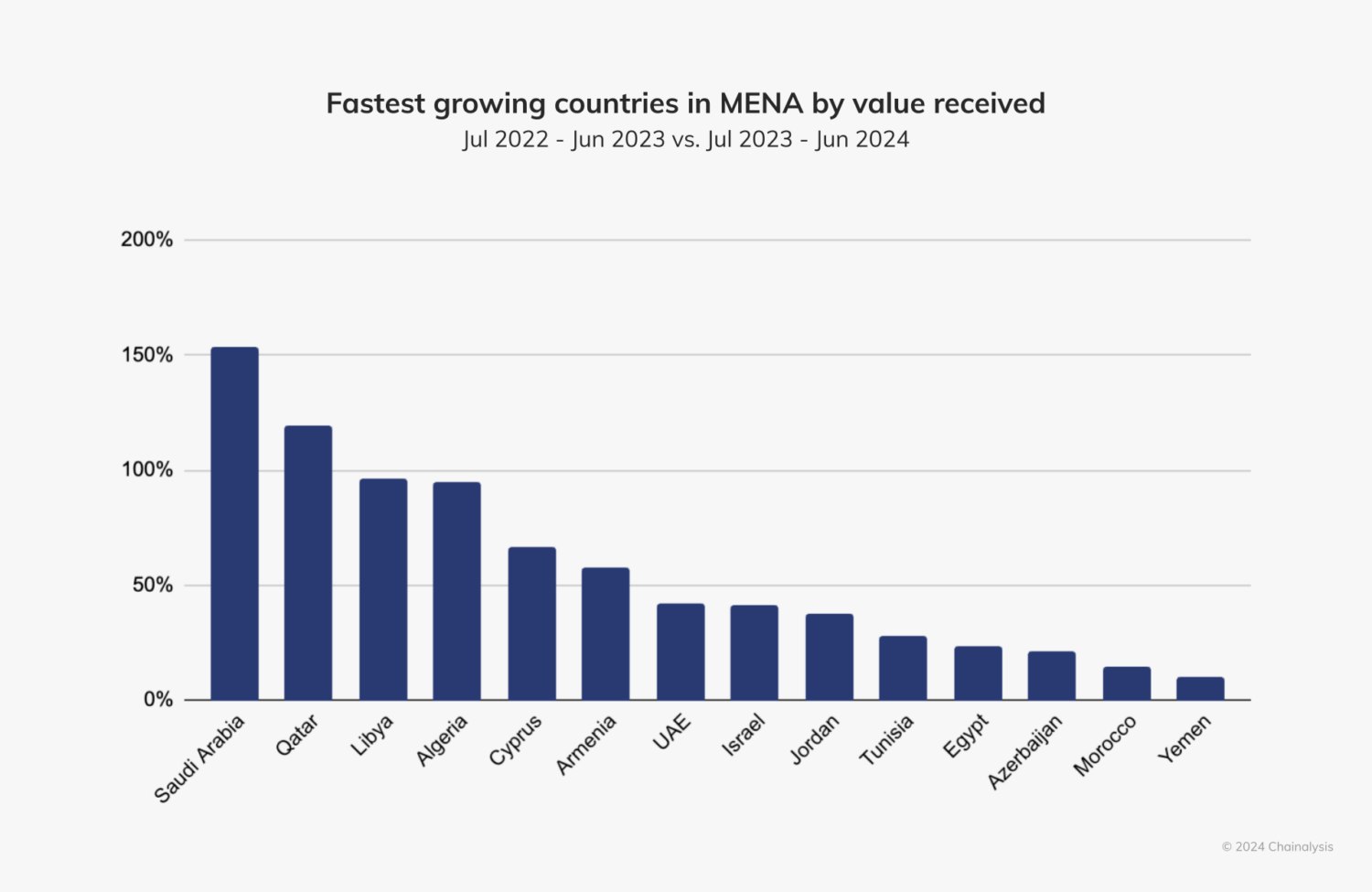

Saudi Arabia and Qatar are MENA’s fastest growing crypto economies

Like last year, Saudi Arabia remains the fastest-growing crypto economy in the MENA region — growing by 154% year-over-year, with a focus on blockchain innovation, central bank digital currencies (CBDCs), gaming, and fintech innovation more generally.

Several traditional financial (TradFi) powerhouses like Rothschild and Goldman Sachs have recently set up shop in Riyadh, joining Lazard, who has maintained a presence in the country since 2011. As adoption accelerates, TradFi institutions are increasingly courting crypto — Goldman Sachs plans to launch three tokenization projects globally by the year’s end. Saudi Arabia’s young population and growing interest in crypto is an opportunity to develop talent and innovation in the digital finance space.

Qatar follows closely as the region’s second fastest-growing market, growing by 120% year-over-year, along with its regulatory stance evolving. The launch in September of a new digital assets regime by the Qatar Financial Centre (QFC), establishes legal and regulatory foundations for digital assets, asset tokenization and trusted technology infrastructure to develop, paving the way for accelerated fintech innovation, contributing to the country’s digital transformation journey.

As countries like Saudi Arabia and Qatar continue to experience rapid growth in adoption, there is an opportunity for regulatory frameworks to develop alongside this dynamic landscape. As consumer demand and market activity increases, regulatory clarity can foster innovation, provide stability for businesses and attract investors.

Charting MENA’s global impact

MENA is rapidly emerging as a key player in the crypto economy of the world. The region’s growth, fueled by institutional and enterprise activity, along with a strong appetite for DeFi and stablecoins, points to a likely expansion of MENA’s influence in the crypto space. While CEXs still dominate, the rise of DeFi is also reshaping the landscape with nations like Saudi Arabia and the UAE embracing decentralized platforms. This underscores DeFi’s potential to drive financial inclusion across MENA, especially given the substantial underbanked population in the region at large.

Stablecoins and altcoins have also gained traction, especially in countries like Türkiye, where the economic environment has made stable stores of value desirable. Meanwhile, the UAE has positioned itself as a swiftly maturing and balanced crypto ecosystem, thriving under a regulatory framework that encourages innovation and a broad spectrum of local and international market participants.

Looking ahead, the regulatory strides made in 2024 will be crucial in shaping the future of crypto in MENA. As blockchain technology, tokenization, and cryptocurrency become more integral to the global financial landscape, these fast-growing markets will benefit from providing further legal and regulatory certainty to sustain growth and attract international interest, solidifying MENA’s increasingly prominent role in the global crypto ecosystem.

This website contains links to third-party sites that are not under the control of Chainalysis, Inc. or its affiliates (collectively “Chainalysis”). Access to such information does not imply association with, endorsement of, approval of, or recommendation by Chainalysis of the site or its operators, and Chainalysis is not responsible for the products, services, or other content hosted therein.

This material is for informational purposes only, and is not intended to provide legal, tax, financial, or investment advice. Recipients should consult their own advisors before making these types of decisions. Chainalysis has no responsibility or liability for any decision made or any other acts or omissions in connection with Recipient’s use of this material.

Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information in this report and will not be responsible for any claim attributable to errors, omissions, or other inaccuracies of any part of such material.